Your credit score may limit the amount of loan that you can obtain. It is one of the most important factors in determining what your monthly car payment will be for those that finance without a large down payment.

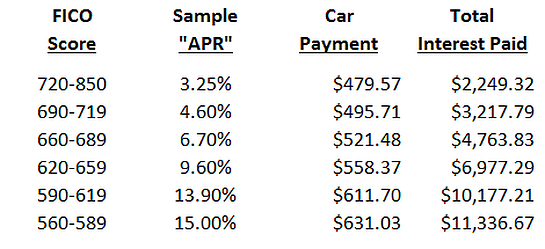

The chart below provides an example of how your credit score can impact the “APR”, the monthly loan payment and the amount of interest that you will have to pay over the “Term” (assuming a $32,000 vehicle, $2,500 down payment, $5,000 “Trade-In”, 60 month loan and 7.5% sales tax rate):

-

(Expert Tip) Only buy an automobile that you can afford. Estimate how much you can spend by using the Affordability calculator.

-

(Expert Tip) Know your credit score. Utilize one of the free credit score providers such as Credit Karma and Annual Credit Report to get started. A poor credit score such as one below 550 will make it difficult to obtain financing without a large down payment. Knowing your actual credit score will make it much easier for you to negotiate the best finance rate. (Please note: Most lenders will use your FICO score. Many of the free credit score services will not provide you with a FICO score but will provide you with a good idea of the credit category that you fall into.)

-

(Expert Tip) If you have a low credit score, consider delaying your new vehicle purchase for several months in order to clean up your credit history and to investigate any inaccurate information.

-

(Expert Tip) Get pre-qualified for a loan from your bank, credit union or a trusted affiliate such as Bankrate before you even step foot in a dealership. You will then know how much you can spend and know exactly what interest rate the dealer would have to beat. Many lenders will negotiate with you on their rates and fees so always ask for a better deal.

-

(Expert Tip) Try to finance no more than 80% of your chosen vehicle’s “Invoice Price” in order to maintain positive equity in your vehicle throughout the “Term”.

-

Since many incentives can’t be combined, it is important to know which choice offers the best value for you. Use the “Rebate” or “Rate Incentive” calculator to find out.

-

Do not take out multiple loans (dip routines) for a vehicle purchase. If you are unable to obtain financing for your chosen vehicle through one source, consider alternatives as outlined in STEP 1.

-

Keep your loan “Term” at 60 months or less (48 months or less on a “Lease”). Shorter “Term” loans allow for you to stay ahead of depreciation and therefore help you avoid having any “Negative Equity”.

-

Choose simple interest rate loans over more complex Rule of 78 rate and balloon-payment loans.

-

Consider bi-weekly loan payments to save on interest and to build up equity faster.